$OSCR Deep Dive

Why Oscar Health Is Now My 3rd Largest Holding

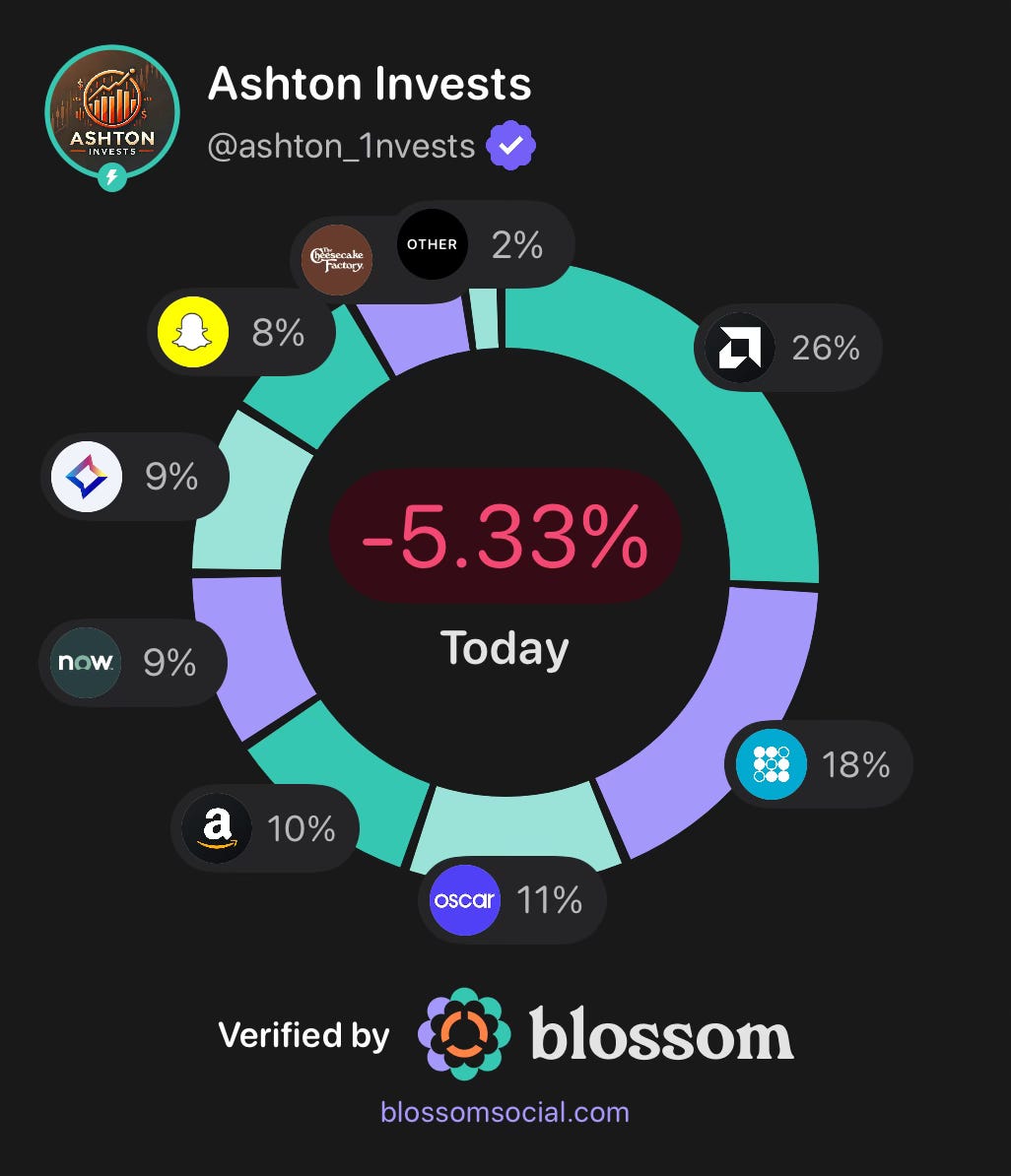

Oscar Health has become one of the most interesting positions in my portfolio. It is now my 3rd largest holding, and while that may sound aggressive to some people, I am comfortable with it because I think the market is still missing the bigger picture.

Oscar is not a perfect company. It operates in healthcare, which means regulation, policy risk, medical cost volatility, and execution risk are all very real. But the opportunity is also real. This is a company growing fast, scaling into profitability, and attacking one of the most frustrating parts of the U.S. economy: health insurance.

What Oscar Health Actually Does

Oscar is mainly focused on the individual and family health insurance market, which includes people buying coverage through the ACA marketplace. That means Oscar serves people who are not getting traditional employer-sponsored insurance, including self-employed workers, freelancers, gig workers, small business owners, families, people between jobs, and early retirees.

That market matters because the way people work is changing. Not everyone has one lifelong employer with one traditional health plan anymore. More people are working flexible jobs, switching careers, building businesses, or choosing independent work. Oscar is built for that world.

The company is trying to make health insurance feel more modern, simple, and consumer-friendly. That sounds basic, but healthcare is still one of the most confusing industries in America. People hate trying to figure out what is covered, what something costs, where to go, who to call, and whether a bill is even correct.

Oscar’s bet is simple: if healthcare is broken and confusing, there is room for a company that makes it easier. That is the core thesis.

Why The Market Opportunity Is Bigger Than People Think

The reason I am bullish is because Oscar is no longer just an interesting idea. It has real scale now.

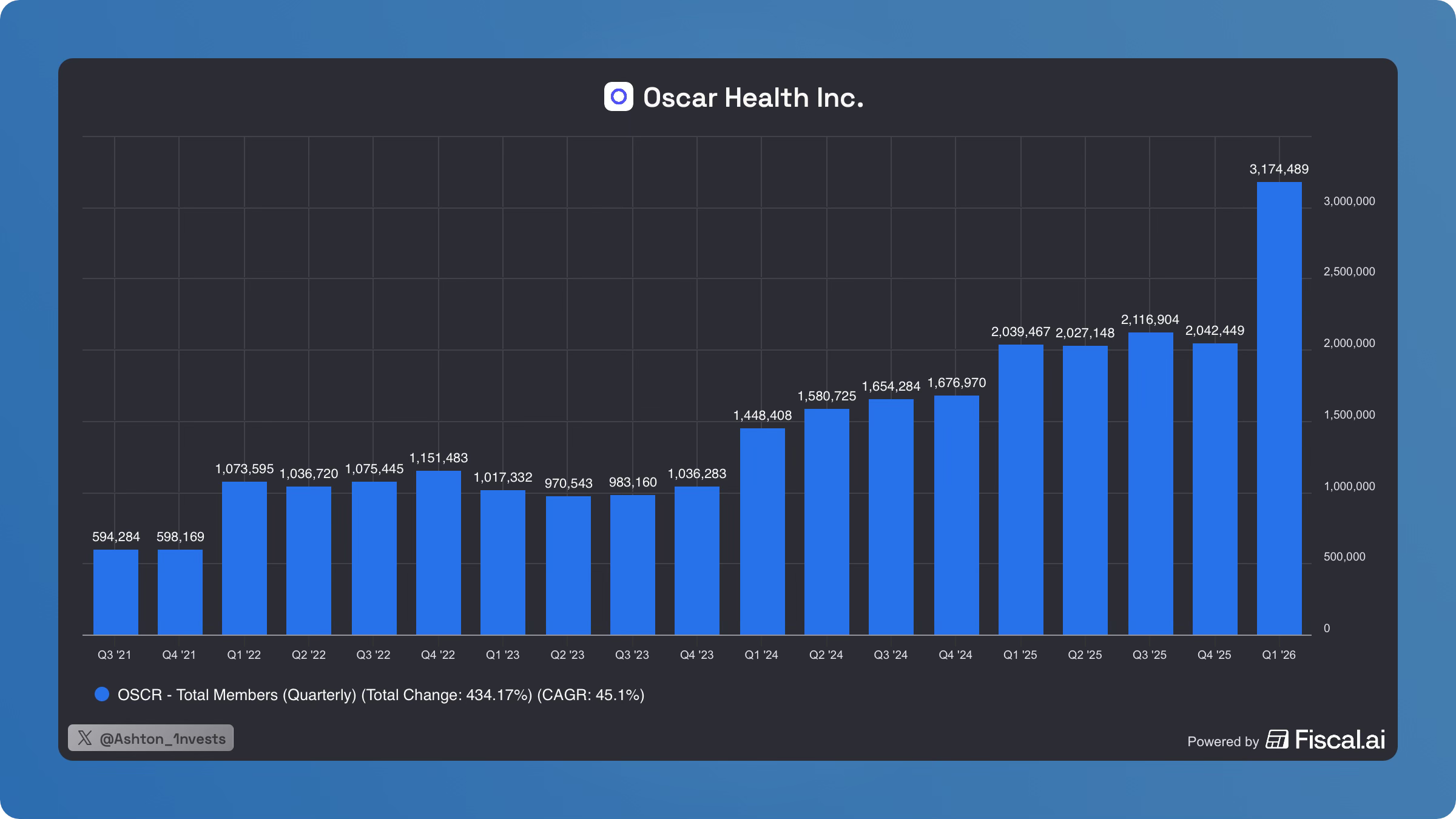

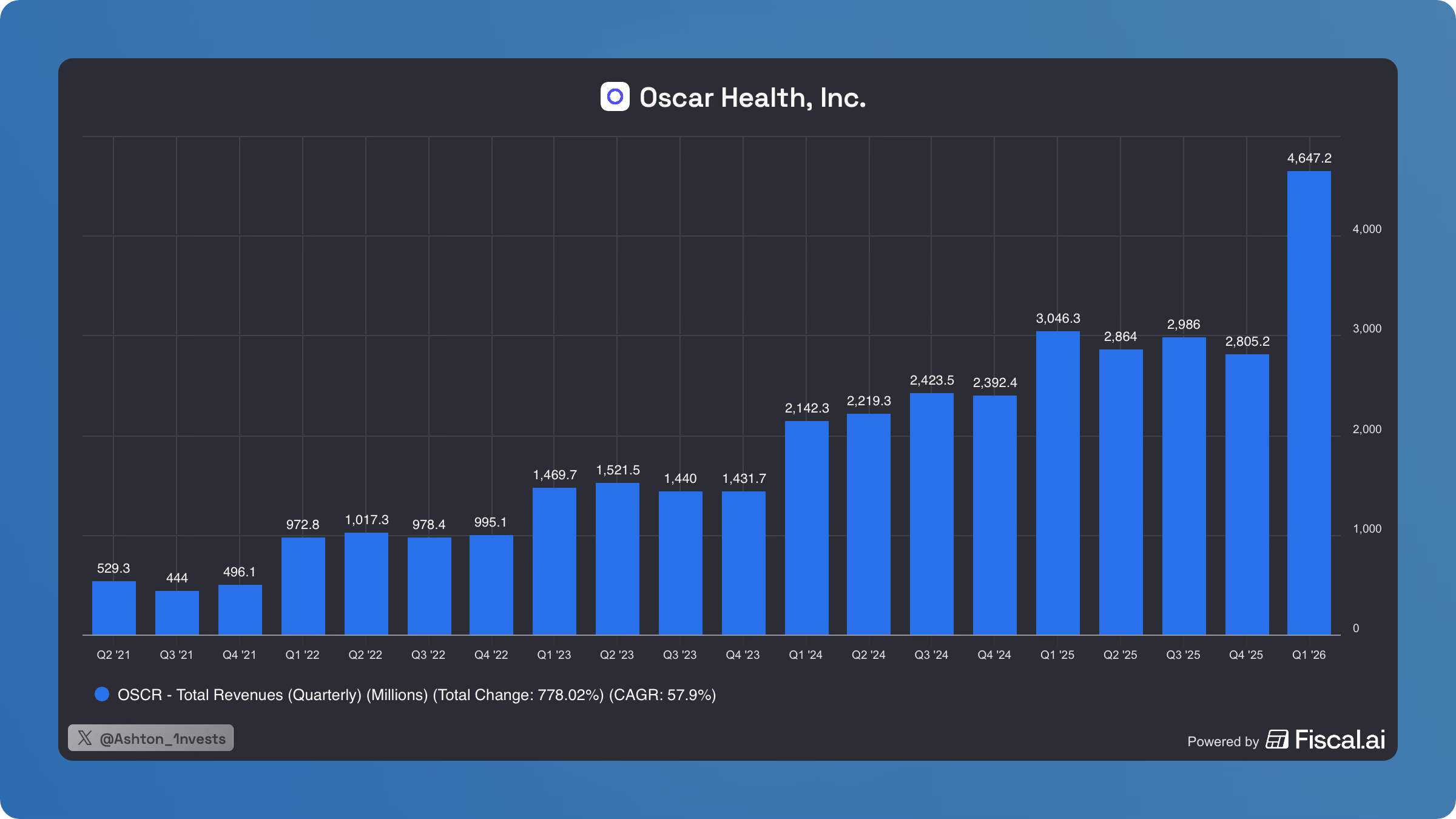

In Q1 2026, Oscar had roughly 3.17 million members, up from around 2.04 million in Q1 2025. Revenue came in at about $4.65 billion, up around 53% year-over-year. That is not small growth. That is a company becoming much larger very quickly.

Scale matters a lot in insurance. More members can mean better data, better pricing, better fixed cost leverage, better provider relationships, better brand awareness, and better efficiency over time. For years, the knock on Oscar was that it was growing but had not proven the economics could work. Now that question is starting to change.

The market is not just asking, “Can Oscar grow?” It is starting to ask, “Can Oscar grow profitably?” That is where the story gets interesting.

Q1 2026 Was A Major Statement

Q1 2026 was a huge quarter for the thesis. Oscar reported $679 million in net income attributable to the company and $727 million in adjusted EBITDA. Medical loss ratio improved to 70.5%, compared to 75.4% in the prior year period. SG&A expense ratio also improved to 15.2%, compared to 15.8% last year.

Those numbers matter because they show what the business can look like when growth, pricing, medical costs, and operating leverage are all moving in the right direction. For a while, $OSCR was viewed as a “growth but no profits” story. Q1 showed that the model can produce real profits when the company executes.

Yes, one strong quarter does not prove everything. Q1 is seasonally strong for health insurers, and Oscar still has to prove this over a full year and through different market environments. But the quarter showed the upside inside this business if Oscar keeps scaling correctly.

Why Medical Loss Ratio Matters

Medical loss ratio is one of the most important numbers for an insurer. In simple terms, it shows how much of premium revenue is being spent on medical claims. If that number gets too high, profitability gets crushed. If it improves, the earnings power can change quickly.

Oscar’s MLR improvement in Q1 was a big deal because medical cost control has always been one of the biggest bear arguments against the company. Bears have said Oscar can grow members, but growth does not matter if the company cannot manage claims and price risk correctly.

That is a fair concern, but Q1 pushed back on that argument. It showed Oscar can produce strong profitability when the model is working. This is one of the numbers I will be watching every quarter.

The Operating Leverage Story

The other part I like is operating leverage. Oscar’s revenue is growing fast, but SG&A as a percentage of revenue is starting to move in the right direction. That is exactly what I want to see from a company scaling.

The dream scenario is simple: members grow, revenue grows, the platform becomes more efficient, expenses become smaller as a percentage of revenue, and earnings grow faster than sales. That is the path to a much more valuable company.

This is also why 2026 guidance matters so much. Oscar is guiding for $18.7 billion to $19.0 billion in revenue, medical loss ratio of 82.4% to 83.4%, SG&A expense ratio of 15.8% to 16.3%, and earnings from operations of $250 million to $450 million.

That would be a massive improvement from 2025, when Oscar generated strong revenue but still posted a full-year loss. In my opinion, 2025 was the reset year. 2026 is the year where they need to prove the model can generate real profitability.

The Valuation Is What Makes This Interesting

Valuation is where this gets even more interesting. Oscar is expected to do close to $19 billion in revenue this year, but the market is still valuing the company like it has a lot to prove.

To be clear, health insurers should not trade like software companies. Margins are lower, regulation matters, and medical costs can be unpredictable. But that is not the bull case.

The bull case is not that Oscar deserves some crazy SaaS multiple. The bull case is that Oscar is being valued like an uncertain healthcare story while the company may be turning into a profitable growth story. That difference is where the upside could come from.

If Oscar can eventually produce even a few percentage points of operating margin on a much larger revenue base, the earnings power could become meaningful. The company does not need perfection. It just needs to prove that the profits are real and sustainable.

The CEO Buying Stock Matters

One thing I also think is worth paying attention to is insider alignment. CEO Mark Bertolini bought 1 million shares at $11.92 per share in April 2026, worth roughly $11.9 million. That is not a tiny symbolic buy. That is a major purchase from the person running the company.

Insider buying does not guarantee anything. CEOs can be wrong too. But I do think it matters when the CEO is willing to put that much personal capital behind the business, especially at a time when Oscar is trying to prove it can turn scale into profitability.

That kind of move tells me management believes in the long-term setup. Again, it does not remove the risk, but it does add conviction to the story.

The ICHRA Opportunity

Another part of the Oscar thesis that I think gets overlooked is ICHRA, which stands for Individual Coverage Health Reimbursement Arrangement. The simple version is that instead of offering one traditional group health plan, employers can give workers money to buy their own insurance on the individual market.

This is still early, but it could become a meaningful long-term tailwind if more employers want flexibility and more workers want portable benefits. Oscar is already built around the individual market, so if ICHRA grows, Oscar could be positioned well.

That fits the bigger picture: more flexible work, more consumer choice, more people shopping directly for healthcare, and more demand for simpler digital insurance experiences. Oscar does not need ICHRA to explode overnight for the thesis to work, but it is another potential growth lever that I think investors should pay attention to.

The Risks Are Real

I am bullish on $OSCR, but this is not a risk-free stock. The biggest risk is policy. Oscar is tied to the ACA marketplace, and changes to subsidies, enrollment rules, risk adjustment, or regulation can impact the business. Enhanced premium tax credits are especially important to watch because they affect affordability and enrollment in the marketplace.

The second risk is medical cost volatility. If claims come in higher than expected, margins can get hit quickly. That is why MLR is one of the most important numbers I will be watching every quarter.

The third risk is competition. Oscar is going up against larger insurers with more scale, more capital, and deeper industry relationships. The fourth risk is execution. Oscar has to keep growing, pricing correctly, controlling costs, improving margins, and hitting guidance. That is not easy.

So yes, $OSCR is risky. But I think the risk/reward is attractive because the company is finally showing numbers that support the thesis.

What I Need To See Going Forward

From here, I want to see member growth remain strong, but not at the expense of profitability. Growth only matters if the company can price risk correctly and keep medical costs under control.

The biggest things I will be watching are MLR, SG&A leverage, profitability, and whether management can hit or beat 2026 guidance. I also want to see Oscar keep building toward something bigger than just another health insurance company.

That last part is important. I do not view Oscar as just an insurer. I view it as a consumer healthcare platform trying to use insurance as the entry point. If they can make healthcare easier, more digital, and more understandable while also improving the economics of the business, the upside is much bigger than what many investors are giving it credit for.

My Bull Case

My bull case is that Oscar keeps growing in the individual market, benefits from long-term ACA and ICHRA adoption, improves pricing, controls medical costs, expands margins, and proves that it can generate consistent earnings at scale.

If that happens, I think the market will stop viewing Oscar as a risky, unproven health insurer and start viewing it as a profitable healthcare growth company. That is when the stock could get re-rated.

The stock does not need everything to go perfectly. It just needs the market to believe the earnings power is real. That is why I am bullish.

Final Thoughts

Oscar Health is not for everyone. It is volatile, tied to healthcare policy, exposed to medical cost risk, and still has a lot to prove. But I think that is exactly why the opportunity exists.

The company has gone from an interesting idea to a real business with millions of members, billions in revenue, improving profitability, and a CEO putting serious money behind the stock.

$OSCR is now my 3rd largest holding because I think the market is still too focused on the old story. The old story was: can Oscar survive? The new story might be: how profitable can Oscar become at scale?

That is the question that matters to me. And if the answer is better than the market expects, I think $OSCR could be one of the more interesting healthcare growth stories over the next few years.

Disclaimer: This article is for educational and entertainment purposes only. This is not financial advice, and I am not telling anyone to buy, sell, or hold any stock. I currently own shares of $OSCR, so I am biased. Always do your own research and make decisions based on your own risk tolerance, financial situation, and time horizon.

Great research!! I never heard of this company, thx for sharing your views!!

Been holding since 14 dollars... what is your thoughts/expectations on where stock price is in 2027?