CoreWeave Deep Dive

Why $CRWV Has My Attention

CoreWeave is one of the most interesting AI companies in the market, but it is also one of the hardest to understand.

The growth is almost unbelievable. Revenue has gone from nearly nothing to billions of dollars in only a few years, and the company now has huge contracts with some of the most important names in artificial intelligence.

But this is not a clean software story.

CoreWeave has to spend enormous amounts of money on GPUs, data centers, power, networking equipment, and financing before it can recognize the revenue tied to that infrastructure. The company is growing extremely quickly, but it is also taking on a lot of debt and producing large net losses.

That is what makes the stock so interesting. The opportunity is massive, but there is very little room for execution mistakes

.

What CoreWeave Actually Does

The simplest way to explain CoreWeave is that it provides cloud computing built specifically for AI.

Companies training large AI models need access to thousands of advanced GPUs. They also need fast networking, storage, cooling, power, and software that can make all of those chips work together efficiently.

CoreWeave provides that full infrastructure.

It is easy to think of the company as someone buying NVIDIA GPUs and renting them out, but that leaves out a lot of the real value. Customers are not just paying for access to chips. They are paying for a working system that can train and run large AI models without wasting expensive computing capacity.

That specialization is CoreWeave’s biggest advantage. Amazon, Microsoft, and Google offer a much wider range of cloud services. CoreWeave is focused almost entirely on demanding AI workloads.

The company is betting that AI infrastructure is becoming specialized enough for a focused provider to win business from much larger competitors.

The Pivot That Changed Everything

CoreWeave originally started as a cryptocurrency-mining company called Atlantic Crypto.

When the economics of mining changed, the founders realized their GPUs could be used for cloud computing instead. That pivot happened at almost the perfect time.

The launch of generative AI created a major shortage of advanced computing capacity. AI companies needed access to huge amounts of GPU power, and the largest cloud providers could not always deliver it quickly enough.

CoreWeave moved aggressively.

It bought hardware, secured data-center capacity, raised financing, and built a close relationship with NVIDIA. That allowed the company to grow much faster than most people probably imagined was possible.

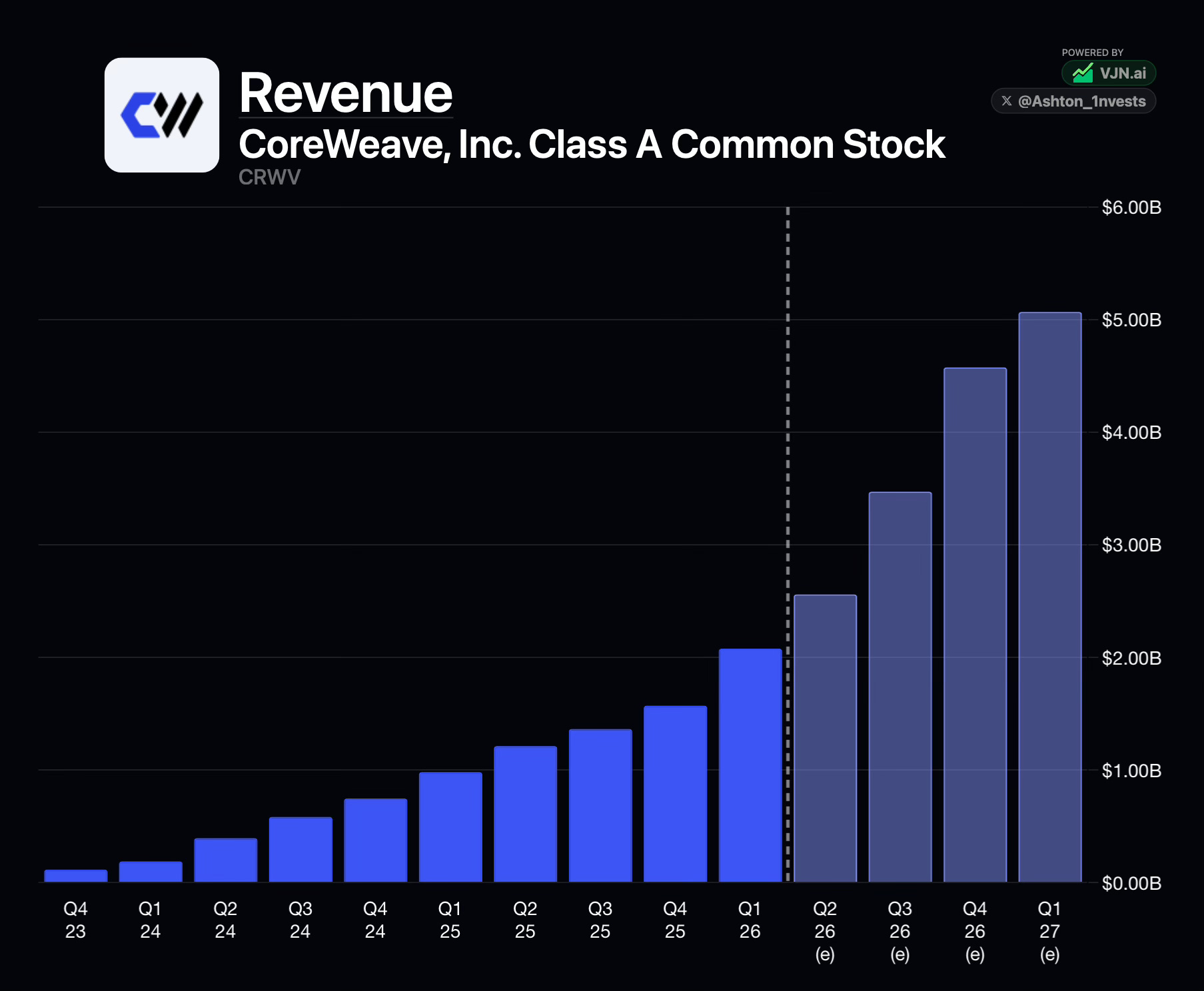

Revenue was only around $16 million in 2022. By 2024, it had reached approximately $1.9 billion. In 2025, CoreWeave generated more than $5 billion, and management expects between $12 billion and $13 billion in 2026.

That growth is the main reason investors are paying attention.

The Demand Is Clearly There

CoreWeave ended the first quarter of 2026 with approximately $99.4 billion in revenue backlog.

A year earlier, that number was around $25.9 billion.

That growth tells us the demand is real. CoreWeave is not depending on small, unproven customers either. It has signed major contracts with companies such as Microsoft, Meta, OpenAI, and Anthropic.

These companies are spending billions of dollars because they need AI infrastructure now. Building it internally can take years, especially when power, chips, and data-center capacity are all limited.

This gives CoreWeave strong revenue visibility, but backlog should not be confused with money already earned. CoreWeave still has to build the infrastructure, bring it online, and successfully deliver the capacity promised to customers.

That is the biggest challenge facing the company.

CoreWeave does not have a demand problem.

It has a delivery problem.

Why Customers Choose CoreWeave

Speed appears to be one of CoreWeave’s most important advantages.

AI companies want access to the newest NVIDIA chips as quickly as possible. Waiting several months for computing capacity can mean falling behind a competitor.

CoreWeave has built a reputation for deploying new NVIDIA systems quickly and operating large GPU clusters built specifically for AI workloads.

The company also offers software that helps customers manage those workloads. Its platform handles storage, networking, monitoring, and coordination across large clusters of GPUs.

That matters because customers are paying for productive computing time. A massive cluster is not valuable if the GPUs are constantly sitting idle because of networking or storage bottlenecks.

CoreWeave is essentially selling speed and efficiency.

For companies racing to build better AI models, both are extremely valuable.

NVIDIA Is a Major Advantage—and a Risk

NVIDIA plays a huge role in the CoreWeave story.

It is a supplier, investor, strategic partner, and customer. That relationship has helped CoreWeave gain access to new hardware and build credibility with major AI companies.

The partnership makes sense for both sides. NVIDIA sells more chips, while CoreWeave becomes another large platform through which customers can access NVIDIA infrastructure.

The risk is that CoreWeave is heavily dependent on one supplier.

If NVIDIA faces delays, changes how it allocates chips, raises prices, or favors other cloud providers, CoreWeave could feel the impact.

Hardware also improves quickly. CoreWeave is spending billions of dollars on GPUs that will eventually be replaced by faster systems.

Older chips will still have value, but CoreWeave needs to earn enough from each generation before the next one becomes more attractive.

That is one of the parts of the business I would watch closely.

The Financials Are Both Impressive and Concerning

CoreWeave reported roughly $2.08 billion of revenue in the first quarter of 2026, up 112% from the prior year.

Adjusted EBITDA came in around $1.16 billion, giving the company an adjusted EBITDA margin of approximately 56%.

Those numbers look incredible at first.

The problem is what happens after that.

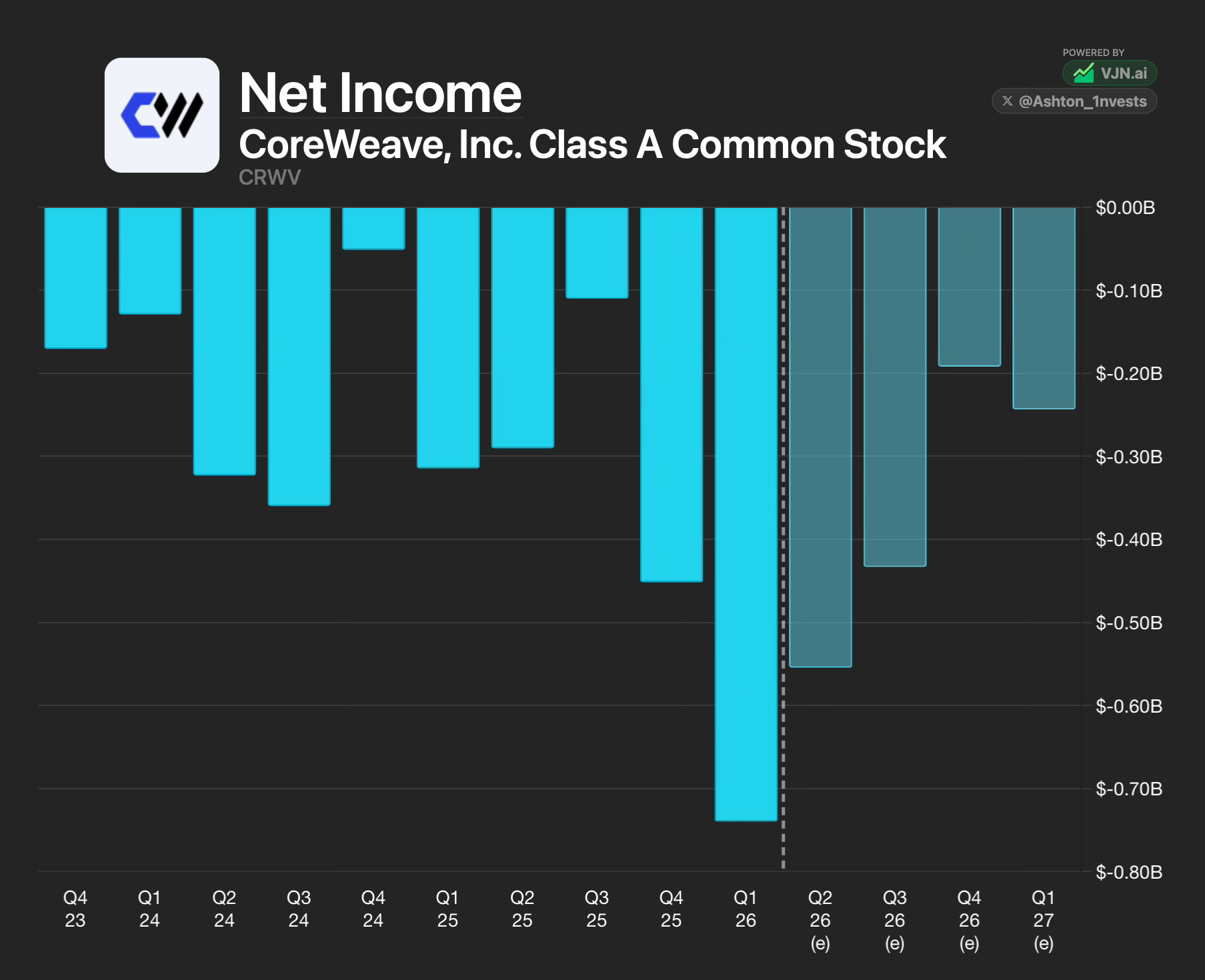

CoreWeave reported an operating loss of roughly $144 million and a net loss of approximately $740 million. Interest expense alone was around $536 million during the quarter.

That is why I would be careful using adjusted EBITDA to value this business.

CoreWeave excludes depreciation and interest when calculating that number, but both expenses are extremely important here. The company owns expensive hardware that loses value over time, and it depends heavily on debt to finance growth.

For CoreWeave, depreciation and interest are not minor accounting details. They are central to the economics of the business.

The company is clearly producing value at the infrastructure level, but it has not yet proven that enough of that value will eventually reach common shareholders.

The Spending Is Massive

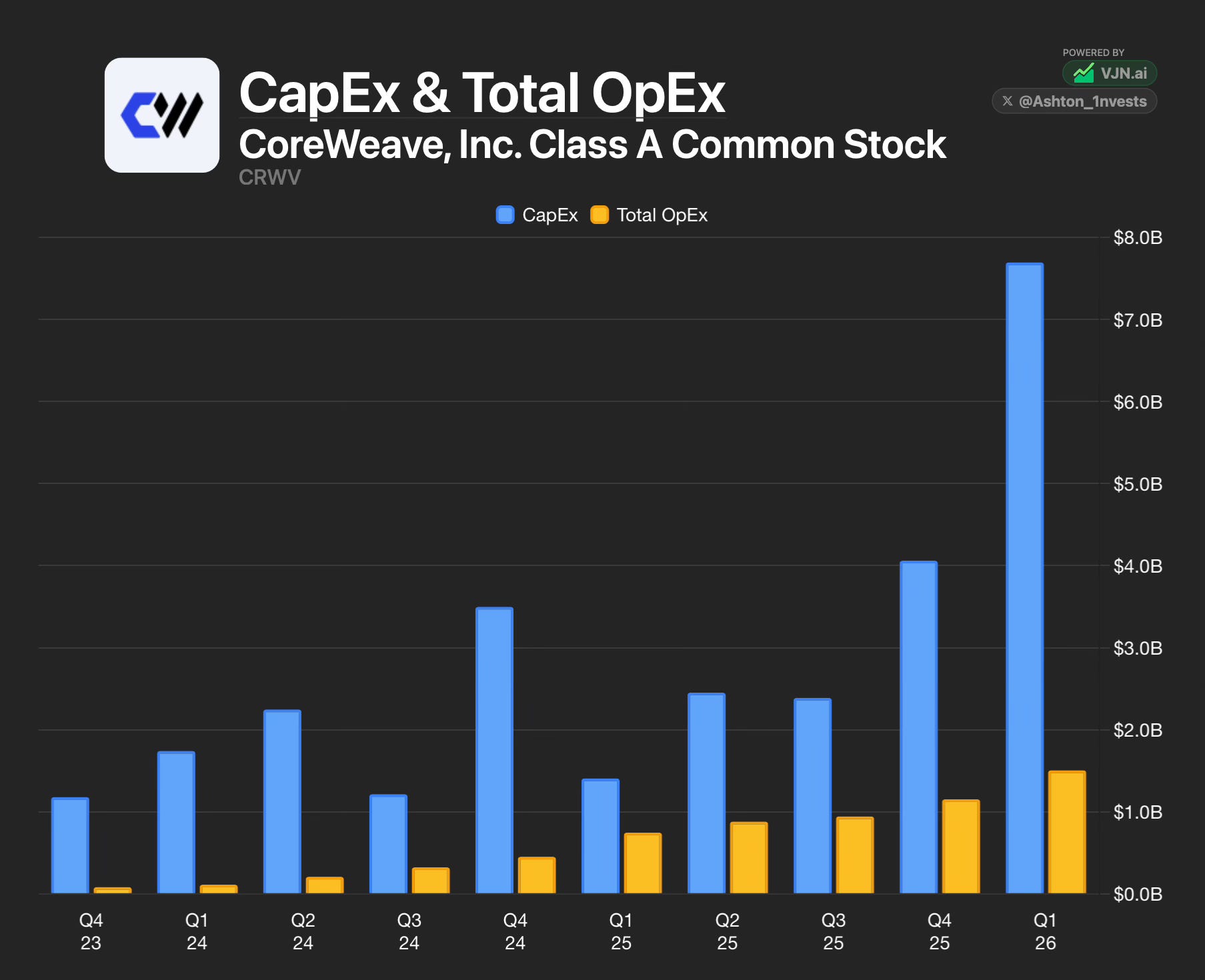

CoreWeave spent approximately $14.9 billion on capital expenditures in 2025.

Management expects to spend between $31 billion and $35 billion in 2026.

That is a massive number for a company expected to generate between $12 billion and $13 billion of revenue this year.

The spending is not completely speculative. CoreWeave has nearly $100 billion of backlog, and much of the infrastructure is being built to serve signed customer commitments.

Still, the company has to spend the money before it collects the revenue.

It has to secure land, electricity, data-center space, GPUs, cooling equipment, networking systems, and financing. Any delay can push revenue into a later period while many of the costs continue.

CoreWeave experienced this in 2025 when a data-center delay caused the company to reduce its revenue outlook.

The contract was still there. The demand was still there.

The infrastructure simply was not ready in time.

Power May Be the Real Moat

Investors naturally focus on GPUs, but power could become just as important.

CoreWeave had more than one gigawatt of active power and over 3.5 gigawatts of contracted power in early 2026. The company believes it could reach more than eight gigawatts by 2030.

Securing that much electricity is not simple. Data centers need access to grids, substations, cooling systems, permits, land, and transmission infrastructure.

These projects can take years to complete.

If AI demand continues growing, companies with access to power may have a real advantage. CoreWeave’s future power capacity could become one of its most valuable assets.

But again, contracted power is not the same as operating capacity. The company still has to build the data centers and bring everything online.

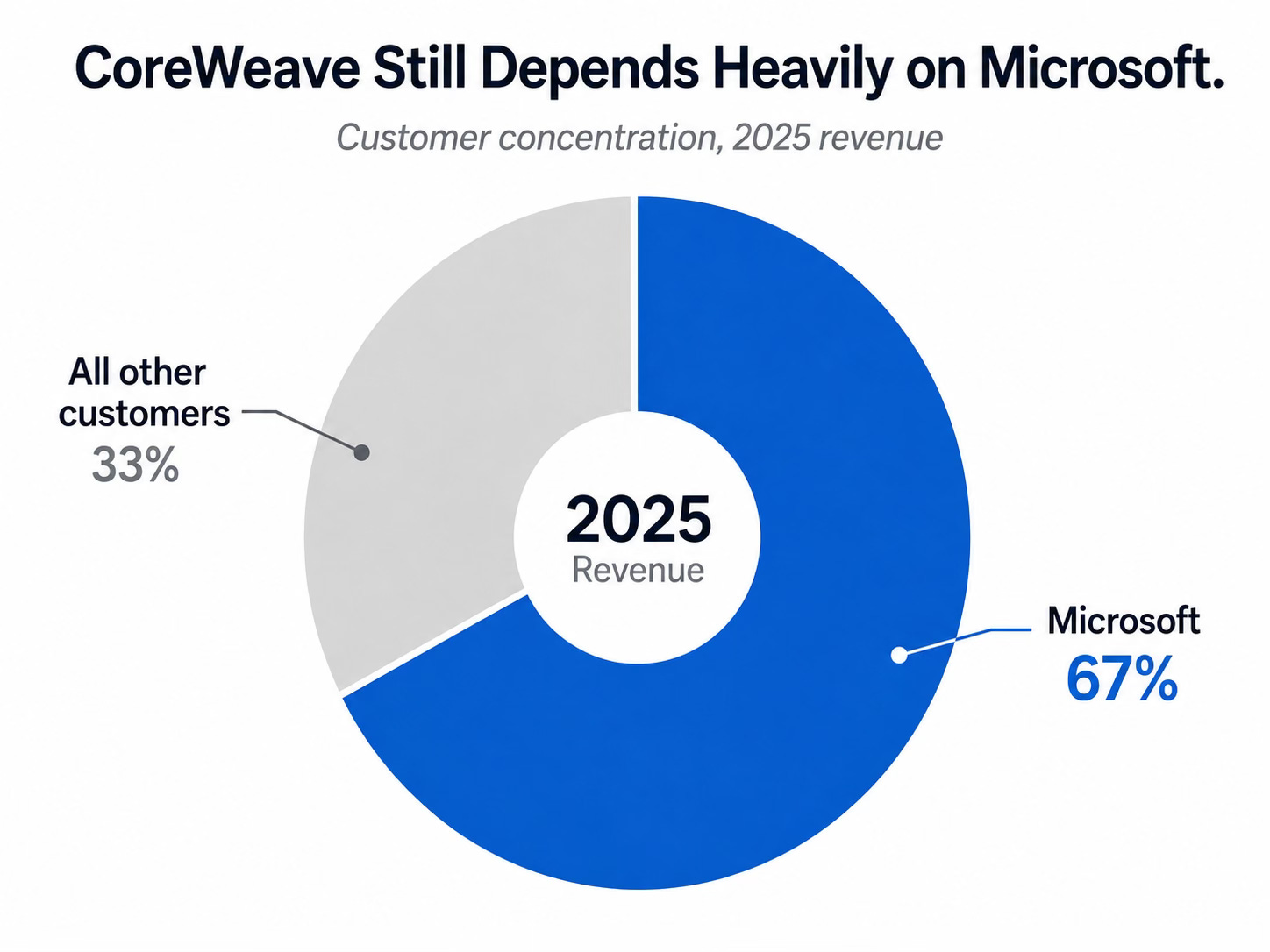

Customer Concentration Is a Real Risk

Microsoft accounted for approximately 67% of CoreWeave’s 2025 revenue.

That is a lot of dependence on one customer.

The good news is that CoreWeave is signing large agreements with Meta, OpenAI, Anthropic, and others. That should make the customer base more diversified over time.

The problem is that many of these customers are also building their own AI infrastructure.

Microsoft, Amazon, Google, and Meta all have the money and technical ability to expand their internal capacity. They may use CoreWeave when they need extra supply or want access to specialized systems, but they may also move more workloads in-house over time.

That makes CoreWeave’s relationships unusual.

Some of its biggest customers could also become its biggest competitors.

The Balance Sheet Is My Biggest Concern

CoreWeave ended the first quarter of 2026 with approximately $24.9 billion of debt, roughly $10 billion of operating lease liabilities, and around $2.2 billion of cash.

The company has used debt, equipment financing, leases, and other arrangements to build its infrastructure.

Some of that financing is tied to specific hardware or customer contracts, which makes it different from a company borrowing money without a clear use for it.

But the debt still matters.

CoreWeave paid more than half a billion dollars in interest during the first quarter alone. That expense could continue rising as the company funds its expansion.

The bull case is that CoreWeave becomes larger, more profitable, and less expensive to finance.

The bear case is that every new dollar of revenue requires even more infrastructure, debt, and interest expense.

CoreWeave eventually needs to show that the business can fund more of its own growth.

Until then, the balance sheet will remain the biggest risk in the story.

Subscribe for more stock deep dives, portfolio updates, and valuation work.

The Bull Case

The bull case is easy to understand.

AI models are becoming more powerful, more widely used, and more compute-intensive. Training still requires enormous infrastructure, but inference could become an even larger opportunity as more people use AI products every day.

AI agents, coding tools, video generation, robotics, scientific research, and enterprise software could all increase demand for computing power.

At the same time, new data centers are difficult to build. Power is limited, construction takes time, and access to the newest GPUs remains valuable.

CoreWeave has already secured major customers, a close relationship with NVIDIA, and large amounts of future power capacity.

If the company keeps converting backlog into revenue, improves margins, lowers customer concentration, and eventually reduces its dependence on external financing, it could become one of the most important AI-infrastructure companies in the world.

What Could Go Wrong

The risk is that CoreWeave is spending as though demand will remain extremely strong for a long time.

That could prove correct, but it also creates a lot of pressure.

AI spending could slow. GPU pricing could fall. Larger cloud providers could increase supply. New hardware could reduce the value of older systems. Construction delays could continue. Interest expense could remain high, and CoreWeave may need to issue more stock.

The worst-case scenario would be slower demand combined with infrastructure commitments that cannot be reduced quickly.

CoreWeave’s debt, leases, and equipment costs do not disappear just because customers need less capacity.

That is why this stock could be extremely volatile.

How I Would Think About Valuation

I would not value CoreWeave using a traditional P/E ratio because the company is not profitable.

A price-to-sales multiple gives us a starting point, but it does not tell the full story either. CoreWeave has much higher capital requirements and debt than a normal software company.

I would rather model what the business could look like in 2028 or 2029.

The most important assumptions are revenue growth, long-term operating margins, interest expense, debt, and dilution.

The stock can work very well if CoreWeave continues growing rapidly and eventually produces strong double-digit operating margins.

It becomes much harder to justify if revenue growth slows while interest expense, depreciation, and capital spending remain elevated.

The real question is not whether CoreWeave can become a much larger company.

It probably can.

The question is how much value will eventually belong to shareholders after paying for all the infrastructure needed to create that growth.

What I Will Be Watching

The first metric I will watch is backlog conversion. CoreWeave already has demand. Now it needs to turn that demand into revenue on schedule.

I will also focus on adjusted operating margin rather than adjusted EBITDA alone. Operating margin gives us a better look at the cost of running this infrastructure.

Interest expense, total debt, capital expenditures, active power, and customer concentration will also matter. I want to see revenue growing faster than financing costs and the company becoming less dependent on Microsoft over time.

The most important long-term question is whether CoreWeave can eventually generate meaningful free cash flow without constantly raising more debt or issuing more shares.

My Current View

I understand the excitement around CoreWeave.

The revenue growth is real. The backlog is real. The customer relationships are real. The company is positioned directly in the middle of one of the largest infrastructure buildouts we may ever see.

I also understand the concern.

CoreWeave is spending enormous amounts of money, carrying a large debt load, and depending on nearly flawless execution. A delay in power, construction, hardware, or financing can quickly affect the results.

I do not see $CRWV as a simple AI stock.

It is a bet that CoreWeave can build one of the largest AI-infrastructure platforms in the world and eventually turn that scale into real cash flow for shareholders.

The upside could be enormous if that happens.

But this is also the kind of stock where I believe position sizing matters just as much as the thesis.

This article is for informational and educational purposes only. It is not financial advice. Always conduct your own research before making an investment decision.

Great Writeup, though I don’t think I’d invest. The sheer amount of debt scares me since even a small hiccup in demand would lead to disastrous consequences.

nicely written