Brookfield Corporation Deep Dive

Why $BN Is Becoming One of My Favorite Long-Term Compounders

Brookfield Corporation is not the type of stock that gets a ton of hype online.

It is not a trendy software company.

It is not a chip stock.

It is not a meme turnaround.

But that is actually one of the reasons I like it.

Brookfield is one of those companies where the thesis is not built around one product, one quarter, or one headline. The thesis is built around assets, capital allocation, cash flow, infrastructure, and long-term compounding.

In simple terms, Brookfield is a global investment holding company with exposure to some of the most important parts of the global economy.

Infrastructure.

Renewable power.

Real estate.

Private equity.

Credit.

Insurance.

Asset management.

Data centers.

AI infrastructure.

Power.

These are not businesses that disappear overnight. These are real assets and financial platforms that can compound over very long periods of time.

That is why I started a position in $BN.

Not because I think it is going to be the fastest stock in my portfolio.

But because I think it can become one of the most durable

.

What Brookfield Actually Does

Brookfield can seem complicated at first, but I think the easiest way to understand it is through three main engines:

Asset Management

Wealth Solutions

Operating Businesses

The asset management business is where Brookfield raises capital from institutions, pension funds, sovereign wealth funds, retail investors, and other clients. Brookfield then invests that capital across real assets, infrastructure, credit, private equity, renewable power, and other long-term strategies.

This is attractive because asset management can be a very scalable business. Brookfield earns fees on the capital it manages, and as fee-bearing capital grows, the earnings power of the platform can grow too.

The Wealth Solutions business is Brookfield’s insurance and retirement platform. This business is important because insurance assets can become a major source of permanent capital. Brookfield can invest that capital into its own strategies and earn attractive returns over time.

The Operating Businesses are the real assets and companies Brookfield owns directly or through its ecosystem. This includes infrastructure, energy, real estate, and private equity assets.

The simple version:

Brookfield raises capital.

Brookfield invests capital.

Brookfield owns real assets.

Brookfield earns fees, distributions, investment returns, and carried interest.

That is the machine.

And the bigger the machine gets, the more powerful it can become.

The Numbers Are Strong

Brookfield’s Q1 2026 results showed why I think the business deserves more attention.

Distributable earnings came in at $1.6 billion for the quarter.

Over the last 12 months, Brookfield generated $6.0 billion of distributable earnings.

Distributable earnings before realizations were $1.4 billion for the quarter and $5.5 billion over the last 12 months.

This matters because Brookfield is not just an asset story. It is a cash flow story.

The company is producing real earnings, real cash flow, and real capital that can be reinvested back into the business.

The Asset Management segment generated $765 million of distributable earnings in the quarter and $2.8 billion over the last 12 months.

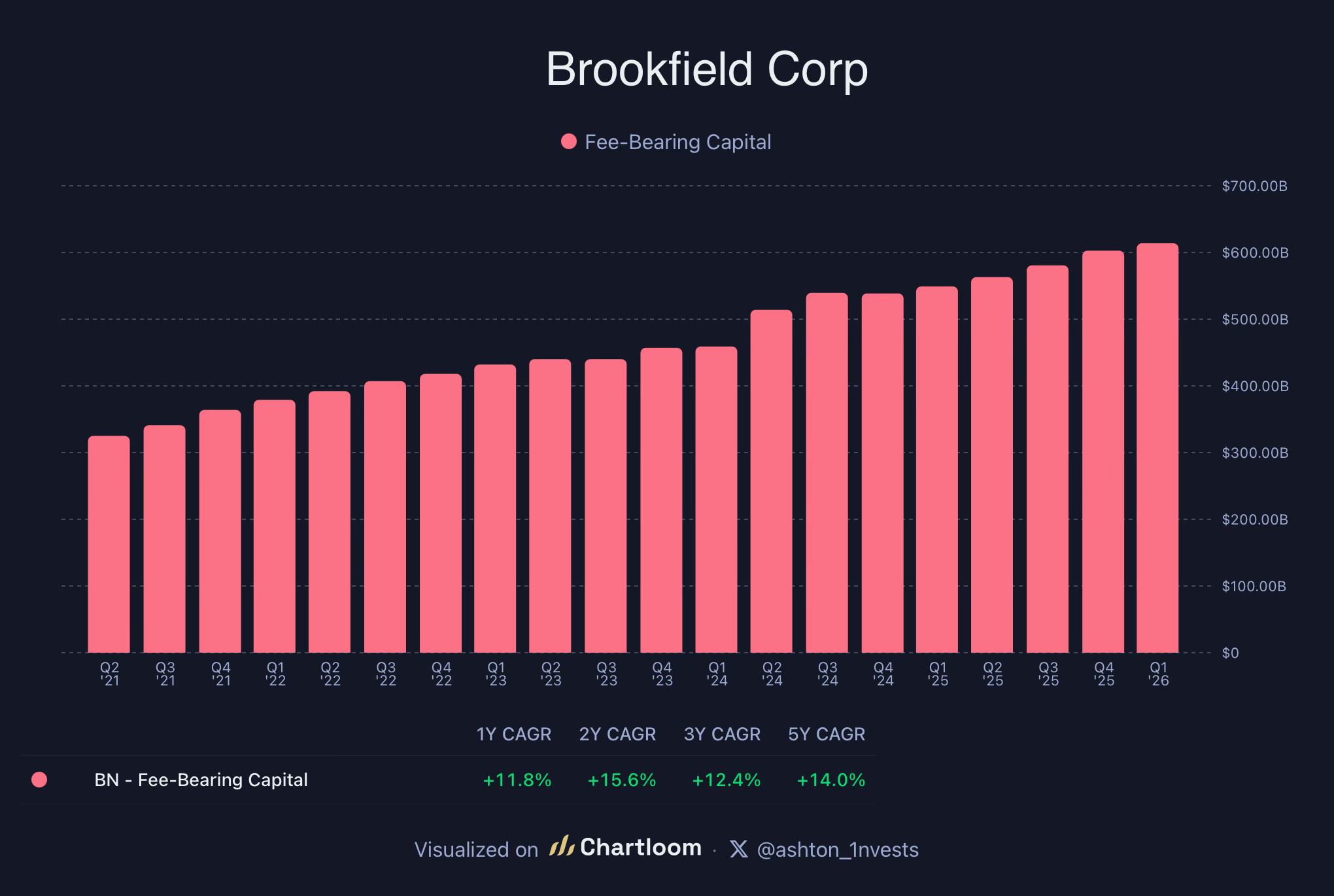

Fee-bearing capital increased to $614 billion, up 12% year over year.

That is a key metric for Brookfield because fee-bearing capital is what supports the long-term growth of fee-related earnings. The more capital Brookfield manages, the more fees the platform can generate.

Brookfield also raised $67 billion year-to-date, including $21 billion in the first quarter.

That tells me demand for Brookfield’s investment strategies is still strong.

This is important because alternative asset managers need capital inflows to keep growing. Brookfield is still attracting capital at scale.

Wealth Solutions Could Become a Bigger Growth Engine

One of the more underappreciated parts of the Brookfield story is Wealth Solutions.

This segment generated $430 million of distributable earnings in the quarter and $1.7 billion over the last 12 months.

Brookfield’s insurance platform is scaling quickly, and the acquisition of Just Group increased total insurance assets to around $180 billion.

That is a big deal.

Insurance gives Brookfield access to long-duration capital. This is capital that can be invested across Brookfield’s platform, creating a flywheel between insurance assets and Brookfield’s investment capabilities.

The company also held $13.2 billion of book equity in Wealth Solutions, generating $2.0 billion in annualized cash flows. Management says that supports a 15% return on equity and values the business around $30 billion.

This is one of the reasons I think Brookfield is more than just a collection of assets.

It is becoming a bigger financial ecosystem.

Asset management brings in outside capital.

Insurance brings in permanent capital.

Operating businesses create real cash flow.

Together, this creates a model that can compound in multiple ways.

The Operating Businesses Add Stability

Brookfield’s Operating Businesses generated $360 million of distributable earnings in the quarter and $1.5 billion over the last 12 months.

This part of the company is not always the easiest to value, but it is very important to the thesis.

Brookfield owns and operates infrastructure, energy, real estate, and private equity businesses that generate cash flow.

These are the kinds of assets that tend to matter in almost any economy.

People need electricity.

Companies need data centers.

Goods need transportation.

Cities need infrastructure.

Businesses need real estate.

The global economy needs capital.

Brookfield sits in the middle of a lot of these areas.

That gives it a level of durability that I really like.

The AI Infrastructure Angle

Brookfield is not the traditional AI stock.

It does not make GPUs.

It does not build large language models.

It does not sell AI software subscriptions.

But AI still matters a lot to the Brookfield thesis.

Why?

Because AI needs infrastructure.

AI needs data centers.

Data centers need land.

They need power.

They need cooling.

They need energy infrastructure.

They need transmission.

They need capital.

And Brookfield is one of the few companies in the world with the scale, relationships, and assets to help build and finance that infrastructure.

Brookfield launched a $100 billion AI infrastructure program in partnership with NVIDIA and the Kuwait Investment Authority.

The initial Brookfield Artificial Intelligence Infrastructure Fund has a target of $10 billion in equity commitments, with the goal of acquiring up to $100 billion of AI infrastructure assets when including co-investors and financing.

This program is focused on the physical backbone of AI.

Energy.

Land.

Data centers.

Compute.

Behind-the-meter power.

AI factories.

This is what I like about Brookfield’s AI exposure.

It is not trying to win the AI race by guessing which app or model becomes dominant.

It is trying to own and finance the infrastructure that the entire AI economy needs.

That is a much different type of AI exposure.

It is less flashy.

But it may also be more durable.

Brookfield Has Massive Capital to Deploy

Another reason I like Brookfield is the amount of capital it has available.

Brookfield ended Q1 2026 with $188 billion of deployable capital.

That includes $74 billion of cash, financial assets, and undrawn credit lines across the corporation, affiliates, and wealth solutions business.

It also includes $114 billion of uncalled private fund commitments.

This matters because Brookfield is at its best when it has capital to deploy during periods of uncertainty.

When markets are calm, everyone wants to buy assets.

When markets are volatile, fewer players have the capital and patience to act.

Brookfield can be opportunistic.

The company invested $53 billion across the business since last quarter and executed $17 billion of asset sales during the quarter.

That is the model.

Buy assets when they are attractive.

Operate them.

Improve them.

Sell or monetize mature assets.

Recycle capital into new opportunities.

Repeat.

Over time, this is how Brookfield compounds.

Management Is Buying Back Stock

One of the biggest things that stood out to me was the buyback activity.

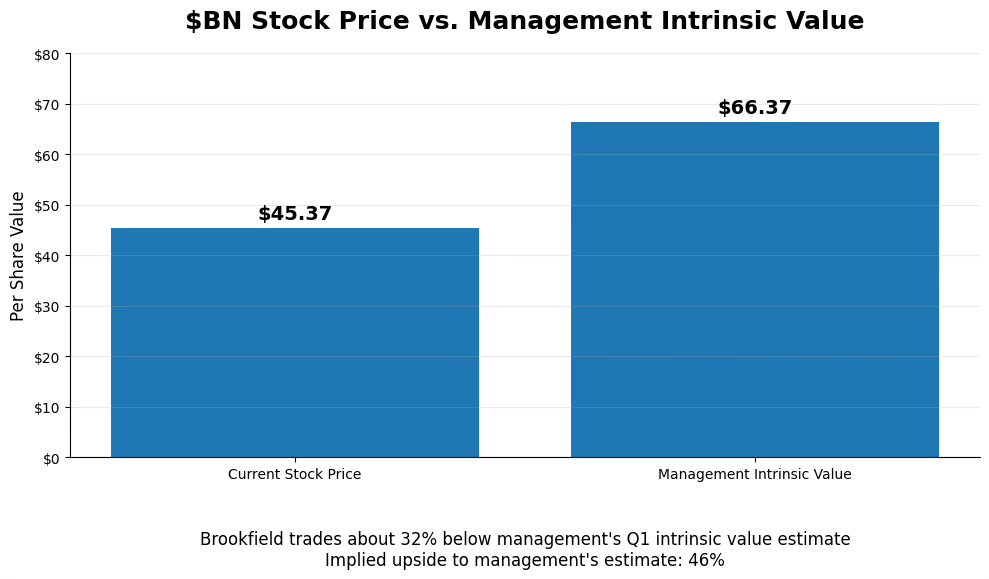

Brookfield repurchased $470 million of BN shares year-to-date at an average price of $41.

Management said that price represented roughly a 40% discount to their view of intrinsic value at quarter end, which was around $66 per share.

That does not mean management’s intrinsic value estimate is guaranteed to be correct.

But it does show how they are thinking.

If management believes the stock is trading significantly below intrinsic value, buybacks can be one of the best uses of capital.

This is especially true for a company like Brookfield, where the gap between public market price and private market value can become a major part of the thesis.

The public market may look at Brookfield and see complexity.

Management may look at Brookfield and see assets, cash flows, capital, and long-term value that are not being fully reflected in the stock.

That is exactly the type of setup I like

The Valuation Case

Brookfield is not easy to value.

That is one of the reasons the opportunity may exist.

This is not a simple P/E stock.

You have to look at asset management earnings, insurance value, operating businesses, carried interest, real estate, infrastructure, energy, private equity, and corporate capital.

That complexity can scare investors away.

But complexity can also create mispricing.

Management’s estimate of intrinsic value was around $66 per share at quarter end.

If the stock is trading around the mid-$40s, that implies a meaningful discount to management’s view of intrinsic value.

Again, I am not saying management’s estimate should be treated as a perfect target.

But I do think it is useful.

Especially when management is actually buying back shares at a large discount to that number.

For me, the valuation case is simple:

Brookfield owns high-quality assets.

Brookfield generates billions in distributable earnings.

Brookfield has a growing asset management platform.

Brookfield has a scaling insurance platform.

Brookfield has massive deployable capital.

Brookfield has exposure to AI infrastructure, power, data centers, real assets, and alternative investments.

And the stock appears to trade below what management believes the business is worth.

That is enough to make it interesting.

Why I Like $BN in My Portfolio

My portfolio already has plenty of higher-upside growth exposure.

I own names like $SOFI, $AMD, $SNAP, $OSCR, and $ZETA.

Those stocks can offer big upside, but they also come with more volatility.

Brookfield plays a different role for me.

$BN is more of a long-term compounder.

It gives me exposure to real assets, infrastructure, AI infrastructure, asset management, insurance, renewable power, private equity, and global capital flows.

It is not the type of stock I expect to move 20% in a week.

But that is not the point.

The point is to own a business that can compound capital over years.

A business that can benefit from multiple long-term trends.

A business that can be opportunistic when markets get volatile.

A business that has real assets and real cash flow behind it.

That is what I want from Brookfield.

The Risks

No investment is perfect, and Brookfield definitely has risks.

The first risk is complexity.

Brookfield is not the easiest company to understand. The structure, different entities, asset classes, and valuation methods can be confusing. That can make it harder for public market investors to fully appreciate the business.

The second risk is interest rates.

Brookfield owns real assets and invests heavily across infrastructure, real estate, credit, and other capital-intensive areas. Higher rates can impact valuations, financing costs, and investor demand.

The third risk is execution.

Brookfield has a lot of moving parts. The company has to keep raising capital, deploying capital, monetizing assets, integrating acquisitions, simplifying its structure, and managing risk across a global portfolio.

The fourth risk is valuation transparency.

Because many of Brookfield’s assets are privately held or valued based on internal estimates, investors have to trust management’s valuation framework more than they would with a simpler public company.

The fifth risk is the AI infrastructure buildout itself.

I like Brookfield’s AI infrastructure exposure, but the scale of investment across data centers and power is massive. If the AI infrastructure boom slows, becomes overbuilt, or sees weaker-than-expected returns, that could impact part of the long-term thesis.

These risks are real.

But I do not think they break the thesis.

They are the risks you accept when investing in a complex, global, alternative asset and real asset compounder.

My Bottom Line

Brookfield is not the easiest stock to explain in one sentence.

But that might be part of the opportunity.

The market loves simple stories.

Brookfield is not simple.

It is an asset manager.

It is an insurance platform.

It is an infrastructure owner.

It is a real estate investor.

It is a power and energy investor.

It is an AI infrastructure play.

It is a capital allocator.

It is a long-term compounder.

And right now, I think the market is still underappreciating how powerful that combination can be.

$BN gives me exposure to some of the most important long-term themes in the world:

Infrastructure.

Power.

AI data centers.

Insurance.

Alternative assets.

Global capital flows.

Real assets.

Long-term compounding.

That is why I started my position.

And from here, I plan to build it slowly over time.

I do not need Brookfield to be the fastest stock in my portfolio.

I need it to be durable.

I need it to compound.

I need it to give my portfolio more balance.

And I think $BN can do exactly that.

Disclaimer: This article is for educational and informational purposes only. This is not financial advice, and it is not a recommendation to buy or sell any stock. I am sharing my personal research and opinion. Always do your own research and make investment decisions based on your own goals, risk tolerance, and financial situation.

I am thinking of buying more